Skip to content

Skip to content

There's never a more frightening time in my life recently then when I became eligible for Medicare. I was inundated with several calls per day and I didn't know what to buy or who to buy it from. I have a friend a little older than me that has been very sick with multiple expensive procedures and tests, he highly recommended this insurance company, Strickland Insurance Group. John Strickland the person for me to see. John came by with a laptop in a PowerPoint he patiently went through everything with my wife and I. He didn't put any pressure on us to buy. My friend had been ill gave high marks so we went that direction and so far very glad we did. Since then another friend who sells supplemental insurance seen my insurance card and told me that I had the best there was out there, so I feel good about our decision and it's worked well so far.

Dale McClellan

Dale McClellan

Mr. Strickland with Strickland Insurance Group came to our home and explained everything to me and my husband. The different types of Life Insurance (I didn’t realize there was several types to choose from). I’m glad we decided to purchase Life Insurance and realized we should have got it years ago. If you are unsure what you need or what type of insurance you need make an appointment with Mr. Strickland you will not be disappointed!

Donna & Steve Hapney

Donna & Steve Hapney

John Strickland is "Johnie on the spot." Whether you are calling for a quote or just to ask a question he is quick to satisfy your needs. You can be confident knowing he will find you the best insurance for your situation and at a very fair price. Put your confidence in a man who cares to fulfill your needs. I never hesitate to recommend John Strickland with Strickland Insurance Group to my friends and family both in Florida and Georgia.

Jill & Dale Chaves - Georgia

Jill & Dale Chaves - Georgia

Keller Williams South Tampa

Anastasia Fischer

3502 Henderson Blvd

Tampa, F 33609

813-597-4791

Email: www.fischergrouptpa.com/contact-form/

Bizzee Bee Marketing LLC

Owner: Georgianna Strickland

Website:

https://bizzeebeemarketing.com

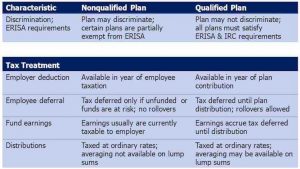

What are Qualified and Non-Qualified Retirement Plans?

In simplest terms, a qualified retirement plan is one that meets ERISA guidelines, while a non-qualified plan falls outside of ERISA guidelines. Qualified plans include

What are Annuities?

An annuity is a type of policy issued by an insurance company designed to accept and grow funds, and upon annuitization, create a stream of

What is Disability Insurance and How does it Work?

Disability insurance replaces a portion of employee income when they can’t work because of an illness or disability. For the most part, disability insurance will